Key Takeaways

- Trump‑era rollbacks of industrial decarbonization grants and low‑carbon procurement programs are slowing the scale‑up of clean cement, as illustrated by Sublime's halted plant and layoffs.

- Surging data center construction is emerging as a critical lifeline for low‑carbon concrete, with hyperscalers offering large, multi‑year offtake commitments that partially offset weakened federal support.

- Low‑carbon concrete has demonstrated it can meet demanding data center performance requirements while delivering meaningful embodied‑carbon cuts with limited cost increases; Meta's Rosemount project shows these advanced mixes could scale and anchor more durable demand for clean‑cement producers.

Low‑carbon cement producers are being squeezed by retreating public support, but a powerful new customer is emerging. The rapid build‑out of AI data centers is creating a concentrated, long‑term demand pool for lower‑carbon concrete, turning these projects into a potential anchor market that can help clean‑cement producers scale on the strength of private investment rather than federal subsidies and projects.

The environmental impact of data centers

According to the International Energy Agency (IEA), data centers use nearly two million liters of water daily. This consumption equals the consumption of 6,500 households. According to the Electric Power Research Institute, in 2023, data centers accounted for 26.0% of Virginia's electricity usage and large shares in various other states, including 15.0% in North Dakota, 12.0% in Nebraska, 11.0% in Iowa and 11.0% in Oregon.

Data centers not only impact the environment during operation, but their construction also requires massive amounts of carbon-intensive materials. Concrete use during these projects can account for as much as 80.0% of total embodied carbon. Although cement typically makes up only 10.0% to 15.0% of a concrete mix by weight, it is responsible for 85.0% to 90.0% of these projects' greenhouse gas emissions. According to MIT's Climate Portal, cement production is responsible for nearly 8.0% of global carbon dioxide emissions, meaning that concrete, as the primary end use of cement, accounts for a significant share of global embodied‑carbon emissions. Low‑carbon concrete mixes can deliver up to 35.0% lower embodied CO₂ than standard concrete.

In an effort to reduce the environmental impact of data centers, large tech companies have sought out deals with low-carbon concrete producers. For example, Amazon has entered into a commercial agreement with low-carbon cement startup Brimstone, reserving future volumes of its lower-carbon ordinary Portland cement for use across Amazon building types, including data-intensive facilities. Meanwhile, Microsoft has signed a long-term purchase agreement for up to 622,500 metric tons of Sublime Systems' low-carbon cement products, enough material to construct on the order of 30 professional football stadiums.

Data center construction is full steam ahead

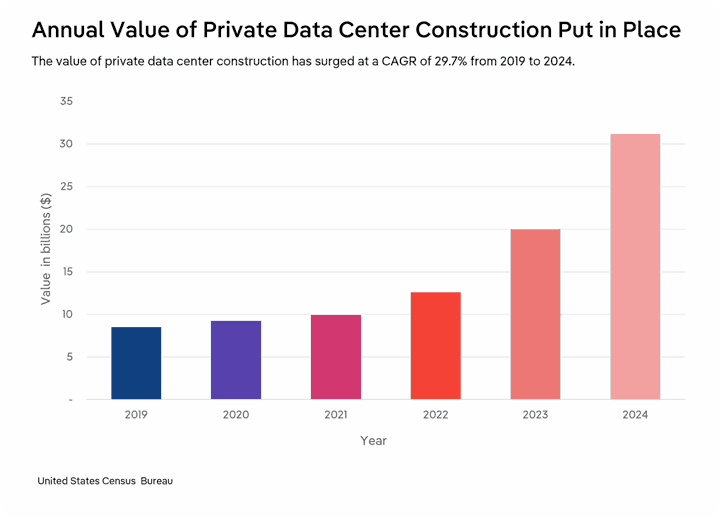

There has been a surge in data center construction in recent years, coinciding with the uptick in AI infrastructure needs. According to census data, the value of data center construction put into place has increased at a CAGR of 29.7% from 2019 to 2024 (latest data available).

This surge in construction spending isn't expected to slow over the near term. Bridgewater estimates that Alphabet, Amazon, Meta and Microsoft will increase AI‑focused capex from $410.0 billion in 2025 to $650.0 billion in 2026.

While a growing number of producers are retrofitting existing ready‑mix and cement facilities to offer lower‑carbon mixes by installing new batching equipment, adding SCM handling and upgrading quality‑control systems, overall supply remains constrained. These upgrades typically convert only a portion of a plant's output to low‑carbon products and often rollout in one region at a time. Hence, industry capacity may fall well short of meeting potential demand from large construction projects such as the current wave of data center builds.

Clean cement projects are hindered by federal funding slashes

The rolling back of federal funding hasn't helped producers expand capacity. In 2024, the Department of Energy awarded $1.5 billion in grants to a handful of large-scale clean cement projects intended to cut process emissions from the cement industry. The Inflation Reduction Act (IRA) also set aside $2.2 billion to help federal agencies procure low-carbon construction materials for new and modernized federal buildings. Together, these programs were designed to both demonstrate next-generation cement technologies and create an early market for lower-carbon materials. The Trump administration has rescinded grants and rolled back IRA-funded industrial decarbonization and procurement efforts, hurting low-carbon cement producers.

In May 2025, the Department of Energy announced that it would cancel more than $3.7 billion in previously awarded funding for nearly two dozen industrial decarbonization projects. Among the affected projects, Sublime Systems had been slated to receive up to $87.0 million to build a commercial‑scale cement facility in Holyoke, Massachusetts, while Brimstone was due to receive up to $189.0 million toward its first commercial plant.

The consequences of these cancellations are already visible in the clean‑cement space. Despite initial plans to continue the build following the announcement of canceled funding, in March of 2026, Sublime Systems paused construction of its planned commercial‑scale plant in Holyoke, Massachusetts and laid off two‑thirds of its staff. However, not all is lost. Despite the grant being pulled, Brimstone is moving forward with its first commercial rock refinery plant, supported by private capital and long‑term offtake interest from customers such as Amazon.

Addressing concerns about widespread construction uses

In addition to capacity constraints, there have been concerns about whether low-carbon cement can be used across the full range of construction needs, especially for critical structural components in data center projects. Recent developments at one of Meta's data center builds have started to address these concerns. An AI-optimized mix developed by Amrize, Meta and the University of Illinois for Meta's Rosemount, Minnesota data center is reported to cut the embodied carbon of the concrete by nearly 35.0% while reaching 4,000-psi strength more than 40.0% faster than the baseline mix.

This mix was not limited to low-risk or small-scale elements; it was used for one of the project's most demanding components, a large structural slab that supports thousands of servers and associated cooling equipment. Its use in this application demonstrated that low-carbon concrete can meet stringent performance requirements without significantly increasing costs relative to conventional cement.

This cost trend has been supported more broadly. A study by Rocky Mountain Institute, drawing on three US building case studies, found that reducing embodied carbon by roughly 19.0% to 46.0% was possible while keeping incremental costs below 1.0% of project budgets. Meta and its partners plan to release the data used to develop the Rosemount mix, which could lower adoption barriers and help similar low-carbon concretes scale across other projects. This proof of feasibility may also spur additional investment in production capacity for comparable mixes, better positioning low-carbon cement producers to serve the rapid build-out of data-intensive facilities without adding considerable costs to the projects.

Final Word

Early successes like Meta's Rosemount project show that performance and cost barriers are surmountable and that deep private demand can begin to substitute for the federal support that has been withdrawn as a driver of scale. Building on this momentum, the strategic opportunity for low‑carbon cement producers now lies in locking in long‑duration commercial contracts with hyperscalers, replicating proven low‑carbon mixes across a broader range of projects and geographies and investing in regional production capacity where data center build‑outs are most intense. By moving quickly to align supply with this concentrated wave of demand, producers can turn today's policy headwinds into a catalyst for market‑led deployment and establish low‑carbon concrete as a core input to the next generation of digital infrastructure.