Key Takeaways

- Insulin is a life-saving drug; the companies that produce it have faced criticism for its exorbitant costs. In 2023, the prices of most insulins were significantly lowered under the Inflation Reduction Act, reducing manufacturer revenue.

- GLP-1s have skyrocketed in popularity. These drugs, initially created as an aid for early Type 2 diabetes, can help patients lose weight. GLP-1s are not subject to a price cap, allowing manufacturers to obtain significant profit.

- The big three manufacturers have begun shifting research focus towards GLP-1s, at the expense of insulin. This has created insulin supply shortages, making it harder for people with Type 1 diabetes to receive the drug.

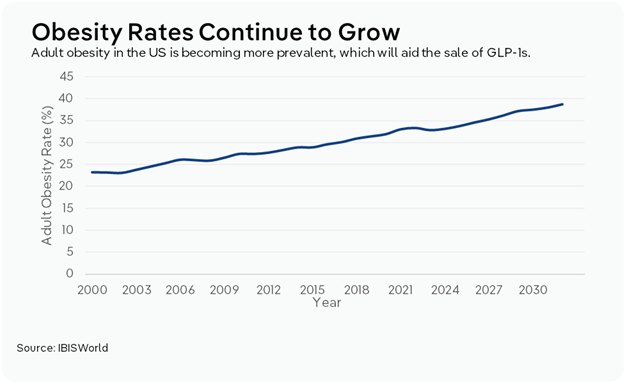

As of 2023, 40.1 million Americans are living with diabetes, 95.0% of them with Type 2, according to the Centers for Disease Control and Prevention (CDC). In the long term, diabetes can lead to heart attacks, strokes, kidney damage and other bodily problems. Since the 1930s, insulin has served as a life-saving solution for diabetics by regulating their blood sugar. However, the once stable market is now being disrupted by the rising popularity of GLP-1s.

GLP-1s, or glucagon-like peptide-1s, have exploded in the mainstream, driven by their effectiveness in treating both Type 2 diabetes and obesity. Drugs like Ozempic and Wegovy have been instilled as a part of everyday culture, in part because of social media and the significant number of celebrities taking the drug. As a result, the drugs have become one of the most dominant growth drivers in the pharmaceutical industry.

As the GLP-1 market has proven profitable, manufacturers that previously focused on insulin have begun to shift towards peptides. However, this reallocation has coincided with reduced funding and the discontinuation of certain insulins, making it harder to secure the medicine for patients who rely on it to survive.

The insulin supply chain: Why did the drug get so expensive?

Insulin has had a history of exorbitant prices. For example, Humalog, one of the most widely used insulins globally, was introduced to the market in 1996, at a cost of $21.23 per 10 mL vial. In 2023, the price of one vial was 1290.0% more expensive, at $274.00. Because of insulin’s necessity, these prices have led to much controversy and, eventually, regulation in the form of a price cap, reducing net profit for manufacturers.

Three manufacturers have dominated global insulin production: Eli Lilly, Sanofi and Novo Nordisk. Together, they have created a highly concentrated market and account for over 90.0% of the insulin production in the US. US-based Eli Lilly and Scandinavian-based Novo Nordisk were among the first companies to manufacture the product, enabling them to achieve economies of scale. That scale allowed them to invest in research, which they used to continuously drive innovation in the drug. Insulin is also a biologic, meaning that it is made from living cells, unlike simple chemical structures. Because of this, it is more expensive to manufacture and must undergo clinical trials to confirm that its chemical structure is similar to those of other products on the market. As a result, large manufacturers are better able to bear the cost of producing the drug. Because of their concentration, these manufacturers can artificially inflate the price of the drug, though those costs are also driven up through the supply chain.

In the 1960s, insurance companies began to offer prescription drug plan (PDP) coverage to their members. Pharmacy benefit managers, or PBMs, were initially created to help insurers manage the administration of PDPs. In the US, PBMs negotiate sales between manufacturers and insurance companies to determine which drugs end up on each insurance company’s formulary, a list of drugs that dictates which medications health plans cover. These companies get a cut of the sales, giving them an incentive to negotiate high prices. They often reward manufacturers that can offer more aggressive rebates, or money back on a drug, with preferred placement on a formulary. A higher list price on a drug can often mean a high rebate for a PBM. This has led to high insulin costs, with the average out-of-pocket cost for insured patients at $58 and for uninsured patients at $123, according to a 2023 study in the National Library of Medicine.

The high cost of insulin has drawn significant pushback from patients, pharmacies, doctors and the government. Public calls for drug price regulation ultimately culminated in the Inflation Reduction Act of 2022. As part of the act, insulin for seniors on Medicare was capped at $35.00 a month. The Biden administration stated its intent to make this price cap available to all Americans, though little progress has been made under the Trump administration. Under the act, drugmakers are also penalized for hiking prices above inflation, so lowering the drug's price allowed them to retain profit on products purchased by Medicaid beneficiaries. This legislation forced all three major manufacturers to cut list prices for many insulins by up to 80.0% in 2023 and capped patients' out-of-pocket costs at around $35.00 a month.

While the decision to cut the list prices of insulin negatively impacted manufacturer revenue, the PBM supply chain was preventing the drugmakers from retaining profit from insulin anyway. However, cutting list prices also meant manufacturers could not offer PBMs high rebates, making PBMs less willing to add insulin products to their formularies, which led to lower use of those drugs. In early 2024, Novo Nordisk stated that it would stop selling its long-acting insulin Levemir in early 2024, in part because of a 60.0% decline in patient access across formularies.

Why have manufacturers shifted focus to GLP-1s?

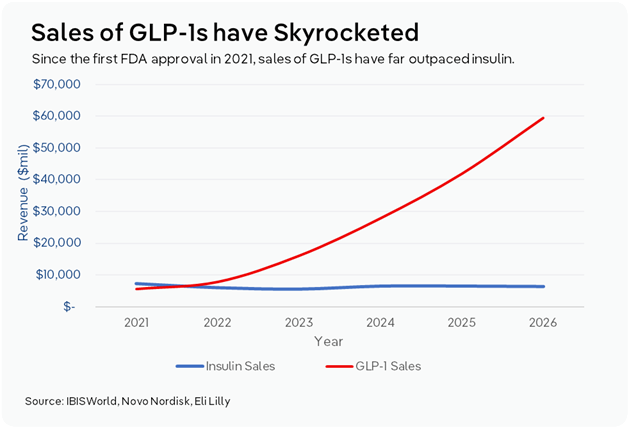

At the same time that insulin prices became the subject of heavy federal regulation, GLP-1s began gaining visibility in the market. GLP-1s were first introduced in the mid-2000s as a treatment for type 2 diabetes to control blood sugar. However, during clinical trials, manufacturers also realized that the drug helped patients lose weight. GLP-1s work differently from traditional insulin in that they slow the movement of food from the stomach into the small intestine, thereby leading patients to eat less. In mid-2021, the first GLP-1 for weight loss, Wegovy, was approved. Since then, consumer interest in the product has skyrocketed. Most insurance plans have begun covering the product for weight loss and obesity.

GLP-1s are considered less medically necessary than insulin because they rely on the body’s ability to produce insulin, so there have been fewer calls to institute a price cap. This means that, even operating through the same PBM supply chain, manufacturers have been able to retain significant profit by selling the drugs. According to the University of Chicago, GLP-1s can cost roughly $700-$800 per month. In some cases, this had led producers to place their focus on these drugs at the expense of insulin. For example, Novo Nordisk, which launched the first FDA-approved GLP-1s, Wegovy and Ozempic, saw its stock price rise by over 400.0% from pre-pandemic levels, according to a 2024 article from the Medical University of South Carolina. In November 2024, Novo Nordisk also announced that it would gradually end production of human insulin pens between 2024 and late 2026, and that process is still underway.

How has a focus on GLP-1s created insulin supply shortages for Type 1 patients?

Though both Type 1 and Type 2 diabetes result in high blood sugar, their core causes differ. Type 1 is an autoimmune disease where the body stops producing insulin. Type 2 is a metabolic condition where the body cannot use insulin properly. Insulin drugs aid both types by supplementing or replacing the body’s natural insulin, helping cells take up glucose and use it for energy.

GLP-1s differ in that they rely on the body’s own production of insulin to promote more effective use. While GLP-1s do not fully replace the effects of insulin, they provide many of the same outcomes, such as better glycemic control, weight loss and reduced risk of low blood sugar. People with early-stage Type 2 diabetes can use GLP-1s alone to keep their blood sugar in a safe range, as it helps the body create additional insulin.

GLP-1s can only act as a substitute for people with Type 2 diabetes. Since the drugs do not provide insulin on their own, they are not a sufficient sole substitute for insulin medicine for those with Type 1 diabetes. However, GLP-1s can help people with Type 1 diabetes improve their glucose control and reduce the amount of insulin they need. Currently, researchers are studying the effect of the drug on Type 1 diabetes. An April 2026 study from the Johns Hopkins Bloomberg School of Public Health found that Type 1 patients who took Ozempic or Mounjaro had reduced risks of heart attacks and end-stage kidney disease. Another study done by the Cleveland Clinic in March 2026 found that taking the drug lowered rates of mortality and decreased hospitalizations for Type 1 patients.

However, in the meantime, shifting focus has made it harder for people with Type 1 diabetes to obtain the medicine they need. Mutual aid groups for diabetes patients have seen surges in requests for insulin because of shortages, which have become more frequent as manufacturers discontinue some vials. In 2024, Eli Lilly discontinued its 3-mL vial of Humalog, which is used in hospitals for inpatient care. This trend is expected to continue, as manufacturers see less profit from the drug.

How are manufacturers responding to growing interest in GLP-1s?

As GLP-1s are prescribed more often at soaring prices, insulin has fewer markets to generate revenue from. While insulin manufacturing will continue to see consistent demand from critical markets, such as Type 1 diabetics, advanced Type 2 cases and government contracts, GLP-1s are now receiving the bulk of investor attention and capital spending. Novo Nordisk and Eli Lilly have each opened or committed to opening GLP-1-focused manufacturing facilities in the US, in part because of threatened tariffs by the Trump administration on patented pharmaceutical companies that are not actively building domestic facilities. At the same time, these drugmakers have continued to discontinue different forms of insulin, including Levemire, Humalog/Humulin vials and Ryzodeg FlexTouch.

As major manufacturers shift their focus to GLP-1s, smaller competitors are poised to capture a larger share of the insulin market. For example, Civica Rx is a nonprofit generic drug company founded in 2018 by US health systems and philanthropies. This company launched its own insulin “at the lowest list price” in the current long-acting insulin market in January 2026.

Drugmakers that are early adopters of GLP-1s will be best positioned to capitalize on a new and booming industry. Many smaller manufacturers are developing proprietary GLP-1s to compete with established brands; some are innovating to make treatment more efficient. For example, Structure Therapeutics is developing an oral GLP-1 pill that can be taken at any time, making it easier for patients who may be hesitant about injections. Also, Altimmune is developing a dual GLP-1/glucagon receptor agonist that can simultaneously preserve lean muscle mass, unlike current drugs that tend to erode muscle alongside fat. As more research is poured into the industry, these manufacturers will have the opportunity to differentiate themselves.

Final Word

The evolving insulin and GLP-1 market points to an uneasy balance going forward. For patients with Type 2 diabetes who can reduce their insulin use, the growth of GLP-1s will expand treatment options, but the shift in manufacturers’ focus raises questions about long-term access and supply stability for those who depend on insulin to survive. Currently, those who have relied on now-discontinued insulin pens have had to switch to syringes and vials, which adds the pressure of measuring correct dosages and injecting themselves. As major manufacturers continue their trend of terminating certain insulins, more patients will likely have to switch to older, less safeguarded forms of injecting themselves, according to a 2024 report from StatNews.

GLP-1 manufacturers have also started to face some pushback on pricing. In May 2026, Maryland was the first state to cap the amount that state and local government health plans will pay for Ozempic. While done to regulate government budgets, this could inadvertently lower consumers' out-of-pocket costs for those plans, helping bring down the drug's price. Other states, such as Colorado, have been considering similar caps. Also, in April 2026, Canada approved the first generic Ozempic, after Novo Nordisk’s regulatory exclusivity ended in January. As generics begin to permeate the US, the price of the drug will likely go down significantly.

GLP-1s have played an outsized role in revitalizing revenue that manufacturers previously saw from insulin. As the industry continues to mature, manufacturers will begin engaging in price competition to keep their customer base. At the same time, the next phase of the market will depend on whether the industry can keep insulin reliably available to those who require it to survive.