Key Takeaways

- Natural gas markets are driving the real shock to global industry, even as Brent crude dominates headlines.

- Disruptions near Qatar’s coastline are quietly reshaping the cost of key industrial inputs like fertiliser, aluminium and plastics.

- The ripple effects across manufacturing and shipping are likely to persist long after any ceasefire.

Research and support: Mia Jeremic

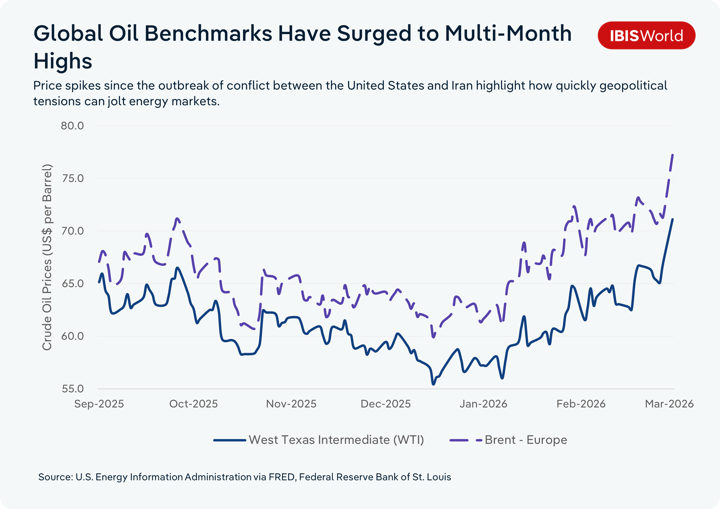

As the conflict between the United States and Iran escalates, headlines have predictably fixated on crude oil. It's the finite fuel underpinning the modern global economy's illimitable quest for expansion. Brent crude has surged past US$100 per barrel, its highest level since January 2025 and tanker traffic through the Strait of Hormuz has all but dried up amid drone strikes and security fears. But while the headlines stick to oil, there's a structurally consequential shock swelling: natural gas.

Trying to separate the impact of oil from gas is largely an academic exercise. Most energy-intensive manufacturers rely on both, whether for fuel or as feedstock. But natural gas is more tethered to pipelines, regional contracts and supply constraints, and it is the foundation of critical industrial processes and the energy transition alike.

Trying to separate the impact of oil from gas is largely an academic exercise. Most energy-intensive manufacturers rely on both, whether for fuel or as feedstock. But natural gas is more tethered to pipelines, regional contracts and supply constraints, and it is the foundation of critical industrial processes and the energy transition alike.

Over the next 12 to 18 months, the industries that will feel the shock most acutely are not oil producers, but fertiliser manufacturers, aluminium smelters, plastics compounders, industrial glass producers and synthetic fibre mills sitting downstream of a gas market that has just been violently repriced. In the United States, higher crude prices will lift pump prices, but a diverse domestic gas supply cushions many industrial users. Europe, meanwhile, is exposed to the ripple effects of a tight global gas market despite its diversified crude imports. Australia, as a major LNG exporter, could see a revenue tailwind even as households and industry face a fresh bout of energy sticker shock.

The immediate pressure may be oil. The more durable industrial story is gas.

Lifting the veil on Qatar's gas cut

On 2 March, Iranian drone strikes forced Qatar to suspend LNG production at Ras Laffan and Mesaieed, triggering a force majeure on gas exports and a full shutdown of liquefaction trains. Even if damage assessments are swift, early indications suggest it will take at least a month to restore normal output, meaning shortages will persist well beyond any immediate ceasefire.

Ras Laffan is the world’s largest LNG export hub. Mesaieed handles a significant share of Qatar’s petrochemical exports alongside LNG. When both facilities go offline at once, the shock runs far deeper than a short‑lived spot price spike.

Qatar supplies predominantly Asian markets, with over 80% of its LNG contracted to buyers in countries like China, Japan and India. There is no like‑for‑like replacement for Qatari volumes. The immediate impacts may not show up overnight in Australian households or European factories but China’s response, whether it chooses to pay up for alternative cargoes, lean on pipeline gas or curb demand, will have a measurable effect on prices and availability across global markets.

Qatar supplies predominantly Asian markets, with over 80% of its LNG contracted to buyers in countries like China, Japan and India. There is no like‑for‑like replacement for Qatari volumes. The immediate impacts may not show up overnight in Australian households or European factories but China’s response, whether it chooses to pay up for alternative cargoes, lean on pipeline gas or curb demand, will have a measurable effect on prices and availability across global markets.

Global LNG markets clear at the margin. When Asian buyers lose access to Qatari cargoes, they bid aggressively for any spare supply. Every alternative reprices upwards, and that repricing ultimately feeds back into contracts, investment decisions and household energy bills far from the Gulf.

Take Australia. It doesn't look like a typical energy‑importing casualty in this crisis. As one of the world's largest LNG exporters, local producers collect a clear windfall when Qatari volumes disappear, and Asian spot prices jump. The problem is that the same price signals that boost export revenue also tighten the screws on gas‑hungry industries. When global LNG prices spike, export terminals naturally attract higher‑paying offshore buyers. The cogs of this market mechanism leave aluminium smelters, glass manufacturers and fertiliser plants on domestic contracts competing with overseas customers for the same molecule. It's a reminder that a shock centred on Qatar’s coastline can still redraw cost curves on the other side of the world.

Thin gas buffers, high food bills

Since the outbreak of the conflict, European benchmark gas prices jumped more than 40% in a single session, with Dutch and British wholesale prices briefly surging by almost 50%. The natural instinct is to map which European countries buy Qatari LNG directly and conclude that those with limited exposure are relatively safe. On this bilateral lens, the United Kingdom appears insulated, sourcing most of its gas via pipeline from Norway and LNG from the United States. The reality is bleaker.

With European storage sitting below 30% of capacity at the end of winter, the buffer heading into this crisis is thinner than at any point in the past five years. In that context, a rerun of 2022‑style margin compression for gas‑intensive users is not a tail risk. If the Strait remains closed for more than a month, it becomes the base case.

The last energy shock showed how quickly this can escalate. Average global fertiliser prices almost tripled between early 2020 and late 2022 as gas costs surged, forcing European fertiliser producers to curtail as much as 70% of capacity at the worst point. Nitrogen fertilisers are particularly exposed because natural gas is both the main energy input and the key feedstock for ammonia and urea, accounting for the bulk of production costs. A disruption to Qatari LNG, combined with turmoil in the Gulf, squeezes exactly the segment of the market that keeps crops fed and yields stable.

Around two‑thirds of Australia’s urea imports now come from Gulf producers, making local grain growers heavily dependent on a region that is suddenly far less reliable. Higher gas prices and any interruption to Gulf export flows will filter directly into fertiliser costs and availability, with farmers forced to choose between paying more, using less or delaying applications.

The knock‑on effects reach well beyond the farm gate. From aluminium smelters and glass furnaces to food processors and freight firms, higher gas and fertiliser prices push up input costs across the global economy. Few of these industries can pass through sharp cost spikes without sacrificing either volumes or margins, so an LNG shock in the Gulf risks reappearing months later as thinner industrial balance sheets, postponed investment and, ultimately, higher consumer prices.

The knock‑on effects reach well beyond the farm gate. From aluminium smelters and glass furnaces to food processors and freight firms, higher gas and fertiliser prices push up input costs across the global economy. Few of these industries can pass through sharp cost spikes without sacrificing either volumes or margins, so an LNG shock in the Gulf risks reappearing months later as thinner industrial balance sheets, postponed investment and, ultimately, higher consumer prices.

Petrochemicals, plastics and planes

It is not just oil and LNG that matters in this crisis. Middle Eastern producers are among the world’s largest exporters of petrochemical feedstocks, which underpin markets for plastics, synthetic fibres and a wide range of industrial chemicals.

The United States has abundant ethane and other feedstocks, but many new petrochemical investments there assumed a world of stable Gulf supply and predictable global pricing. Capacity expansions that once looked straightforward now face a far more volatile backdrop, with input costs and export markets both in flux.

Airlines confront widening jet fuel spreads just as travel demand remains resilient, putting pressure on fares and margins. At the same time, a defence industrial base already stretched across multiple commitments is likely to see accelerated procurement, supporting order books for aerospace and munitions firms but adding further strain to supply chains and skilled labour pools.

There is, however, a longer-term twist. Petrochemicals account for roughly a tenth of global greenhouse gas emissions, yet their products remain deeply woven into modern consumption. If prices stay elevated and supply remains constrained, the disruption may do more than reshape cost structures; it could sharpen the economic case for cleaner materials, stronger recycling systems, and alternative feedstocks.

Opposite forces, unequal damage: the impact on financial markets

In moments of geopolitical stress, capital seeks shelter. The US dollar and Swiss franc have both strengthened, with the franc reaching multi-year highs against the euro. That flight matters industrially: oil and LNG are priced in dollars. Hence, a stronger dollar immediately amplifies import costs in local currency terms for every economy buying Gulf energy, and emerging-market manufacturers already operating on thin margins. That currency effect can be as damaging as the underlying commodity moves.

Arguably, there's also a longer-term tension running in the opposite direction. A prolonged disruption that structurally reduces the volume of US dollar-denominated energy trade gradually erodes one of the foundational sources of transactional dollar demand. This dynamic won't register in short-term exchange rate moves but matters for long-run reserve currency assumptions.

Central banks across major economies find themselves caught between two forces that won't resolve neatly: fresh energy and food price spikes argue against cuts, while softening growth argues against holds. Westpac's modelling suggests even a one-month Hormuz disruption could add around one percentage point to Australian CPI, and similar dynamics are playing out across Europe and Asia. The resulting policy ambiguity has a direct industrial cost, with businesses deferring capital spending and hiring until the rate outlook clears, compressing business confidence simultaneously across major economies.

A closer look at trade finance

The quieter but more immediate channel is trade finance. As risk premia widens, banks globally are repricing letters of credit, commodity finance lines and working-capital facilities tied to Gulf-linked cargoes. This cost doesn't appear as a discrete line item on income statements, it surfaces as higher interest expense, reduced credit availability and deferred capex, particularly for manufacturers with complex cross-border supply chains. Layered on top, financial regulators and institutions are on heightened alert for state-linked cyber activity, adding an operational risk dimension to the funding pressures that banks and market infrastructure are already managing simultaneously.

Maritime war‑risk premiums were already at six‑year highs before the first strike with the market pricing the odds of disruption. Now that the Strait has effectively closed and confirmed the threat environment underwriters had been modelling, reinsurers in London and Sydney are pushing through a broad repricing of Gulf‑linked cover. Trump has instructed the US development‑finance agency to step in with political‑risk cover and guarantees for Gulf shipping, effectively putting a public backstop where private insurance has become expensive or hard to secure. That may keep some cargoes moving, but it doesn't undo the wider repricing of war risk; it shifts more of that risk onto the US sovereign balance sheet and ties firms that rely on it more tightly to policy decisions in Washington.

Taken together, the currency moves, central bank hesitation, and improvised insurance mean that the real question for industry is no longer whether markets will stay open, but on what terms and how much policy risk they are willing to embed in their funding and supply chains.

Final Word

If this decade has demonstrated anything, it's that systemic risk has become the organising condition of the global economy. The Strait of Hormuz long occupied a curious place in that calculus: universally recognised as critical infrastructure for the international energy system, yet persistently underweighted in the risk frameworks of firms, insurers and policymakers alike. That asymmetry is now being corrected abruptly and at scale. The question confronting markets is not simply where energy benchmarks will settle in the near term, but whether the assumptions underpinning global trade and investment remain tenable when one of the world's most consequential maritime corridors slams shut.

A prolonged conflict will inevitably sharpen the debate over how much of the world's energy system remains tied to fuels that sit at the centre of geopolitical fault lines. For export-oriented economies, the question is whether to double down on volatile rents or accelerate the pivot towards less weaponisable sources of advantage. Geopolitics will shape those choices as much as technology or finance. How China manages its relationships with Iran and other Gulf producers and how Asian economies respond collectively to tighter LNG supply will ripple far beyond energy markets into fertiliser, food, metals, shipping and insurance.

What is emerging is not a neat new order but a slow, uneven re-rating of what it means to depend on oil- and gas-rich states for portfolio returns. Washington's renewed appetite for intervention, from Venezuela to the Gulf, suggests the United States is recalibrating its own energy strategy. Other resource-rich states, from Libya to smaller petro-economies, sit uneasily in that shadow.

Conflict in the Strait of Hormuz has not simply disrupted global trade for a period. It could recalibrate how industrial companies, insurers and investors price the risk of operating in or through the Gulf for years to come. Structural shifts rarely arrive with fanfare and they'll accumulate quietly long after the geopolitical headlines have moved on.